Understanding Healthcare Costs: Deductibles, Co-Insurance, Co-Pays & Out-of-Pocket Maximums

Introduction

Healthcare bills can feel overwhelming, especially when you thought “insurance would cover it.” At Haven Healthcare Advocates, we receive many calls from people frustrated by unexpected hospital bills, denied claims, or confusion about what they actually owe.

While we are certainly not here to defend confusing hospital billing practices or frustrating insurance claim processes, we do believe one thing is incredibly important: understanding how your insurance works.

The truth is, many people pay their monthly premium and assume that means healthcare services are mostly covered. Unfortunately, that is rarely the case. Understanding your deductible, co-insurance, co-pays, and out-of-pocket maximum can help you better prepare financially and avoid surprises.

Table of Contents

Key Takeaways

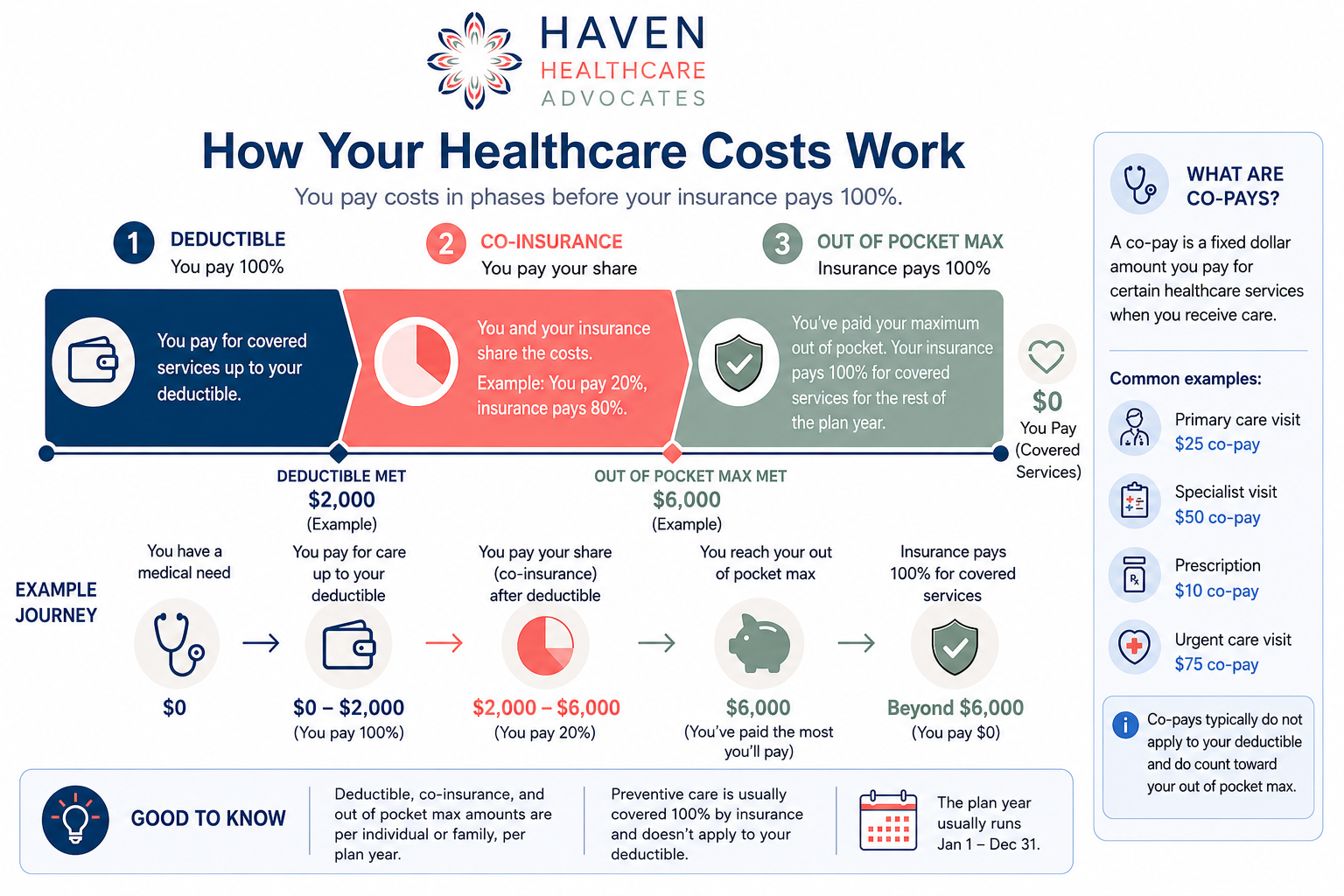

Your monthly premium is the cost to have insurance coverage — it is not the same as healthcare costs.

Your deductible is what you pay first before insurance starts sharing costs.

Co-insurance is the percentage you continue paying after meeting your deductible.

Your out-of-pocket maximum is the most you should pay for covered healthcare services during a plan year.

Co-pays are fixed costs for certain services like office visits or prescriptions.

Premiums typically do not count toward your out-of-pocket maximum.

Insurance plans can become far more complicated depending on network rules, plan structure, and regulations.

Understanding the basics can save you stress, money, and confusion.

What Is a Health Insurance Premium?

Your premium is the monthly amount you pay to maintain your insurance coverage.

Think of it like a membership fee. Paying your premium allows you to access your health plan and may include preventive services such as annual wellness visits or screenings.

However, your premium is not the total amount you pay for healthcare each year.

Once you actually use healthcare services — whether that is a hospital visit, surgery, imaging, or specialist appointment — additional costs usually apply.

Understanding Your Deductible

What Is a Deductible?

Your deductible is the amount you must pay before your insurance starts contributing toward covered healthcare costs.

For example, if your deductible is $2,000, you are responsible for paying the first $2,000 of covered healthcare expenses before insurance starts helping.

If you have a high-deductible health plan and end up in the hospital, it is very possible you could owe the entire deductible amount yourself.

Why Deductibles Matter

Many people are shocked by hospital bills because they do not realize they had not yet met their deductible for the year.

Even though you have insurance, you may still receive a large bill because the deductible phase means insurance has not started sharing costs yet.

What Is Co-Insurance?

Insurance Starts “Holding Hands” With You

Once you meet your deductible, insurance usually begins sharing costs with you instead of paying everything outright.

This shared responsibility is called co-insurance.

A common arrangement is:

You pay 20%

Insurance pays 80%

So if you receive a $10,000 covered medical service after meeting your deductible, you may still owe $2,000 while insurance pays the remaining $8,000.

Important Reminder About Co-Insurance

You are responsible for:

100% of your deductible amount

Your percentage of co-insurance costs until you hit your out-of-pocket maximum

This is one reason healthcare costs can still add up quickly even after insurance begins paying.

Understanding Your Out-of-Pocket Maximum

What Is an Out-of-Pocket Maximum?

Your out-of-pocket maximum is the most you should have to pay for covered healthcare services during a plan year.

Once you hit this limit, insurance typically pays 100% of covered healthcare costs for the remainder of the year.

For many people, this is the financial safety net built into their insurance plan.

Important Note

Your monthly premiums usually do not count toward your out-of-pocket maximum.

That means you continue paying your monthly insurance premium even after reaching your out-of-pocket limit.

Where Do Co-Pays Fit In?

Co-pays do not fit neatly into the deductible → co-insurance → out-of-pocket maximum hierarchy, which is part of why insurance feels so confusing.

What Is a Co-Pay?

A co-pay is a fixed dollar amount you pay for certain healthcare services at the time you receive care.

Common examples include:

$25 primary care visit

$50 specialist visit

$10 prescription medication

$75 urgent care visit

Do Co-Pays Count Toward Your Deductible?

Typically:

Co-pays do not count toward your deductible

Co-pays usually do count toward your out-of-pocket maximum

As we often say — clear as mud.

Why Insurance Gets More Complicated

The reality is that insurance can become much more complicated once you dig deeper.

Some of the additional factors that affect coverage and costs include:

Network Rules

In-network vs. out-of-network deductibles

Different co-insurance amounts depending on provider network status

Plan Structures

Embedded deductibles

Aggregate deductibles

High-deductible health plans (HDHPs)

Employer & Regulatory Differences

Self-funded employer plans

Fully insured plans

ERISA-governed plans

ACA-compliant plans

Non-ACA plans with very different coverage rules

Not All “Coverage” Is Actually Insurance

Some products marketed like insurance are not technically insurance at all and may provide limited protections or benefits.

This is why reading the details of your plan matters so much.Why Medicare Advantage Rehab Denials Happen

Many families are shocked to learn that a patient can be considered “ready for discharge” while still struggling with mobility, medication management, weakness, or cognitive concerns. Just because a patient does not need hospital level of care, does not mean they are ready to go home.

Medicare Advantage plans often use strict authorization guidelines to determine whether inpatient rehab or skilled nursing care will be approved. In many cases, coverage is denied because the plan determines the patient can safely recover at home.

Unfortunately, families and hospital teams may strongly disagree with that assessment.

It is well documented that Medicare Advantage plans are more likely to deny or restrict access to rehabilitation services compared to Traditional Medicare. That can create difficult situations when a patient clearly still needs skilled therapy, nursing support, or supervision.

Final Thoughts

Understanding the basics of health insurance is one of the best first steps you can take to protect yourself financially and avoid unexpected medical bills.

At a minimum, you should know:

Your deductible

Your co-insurance percentage

Your out-of-pocket maximum

Whether your providers are in-network

Healthcare billing and insurance issues can become extremely complex very quickly. If you are dealing with denied claims, confusing bills, out-of-network issues, or overwhelming healthcare costs, working with an advocate can make a significant difference.

At Haven Healthcare Advocates, we help individuals and families navigate the healthcare system, understand their insurance, and fight for fair outcomes.

If you are struggling with a medical billing or insurance issue, reach out to our team. We know the system, and we know the language.

👉 Schedule a consultation with Haven Healthcare Advocates today

We’ll walk you through your options and help you take the next step with confidence.

FAQ’s

What is the difference between a deductible and a co-pay?

A deductible is the amount you must pay before insurance starts sharing costs. A co-pay is a fixed amount you pay for certain services, such as office visits or prescriptions.

Does insurance pay anything before the deductible?

Sometimes. Many plans cover preventive care before the deductible is met. Some services may also have co-pays that apply before meeting the deductible.

What counts toward my out-of-pocket maximum?

Typically, deductibles, co-insurance, and co-pays count toward your out-of-pocket maximum. Premiums generally do not.

What happens after I hit my out-of-pocket maximum?

For covered healthcare services, insurance usually pays 100% of costs for the remainder of the plan year.

Why was my hospital bill so high even though I have insurance?

Common reasons include:

You had not met your deductible

The provider was out-of-network

Certain services were not covered

Co-insurance still applied

The claim was denied or processed incorrectly

Should I appeal an insurance denial?

Yes — many insurance denials are overturned on appeal. Understanding your plan and the denial reason is critical. An advocate can help guide you through the process.